The “No Fee” Lie That Is Costing You Thousands

Most people are idiots when they travel. I say that with love, but it’s true. They work 60 hours a week to save $5,000 for a trip to Europe or Asia. Then, the moment they land, they light 5% of that money on fire.

They walk up to a currency exchange booth at the airport. Or they use their standard Chase or Bank of America debit card at an ATM. They see “0% Commission” plastered on the screen. They feel smart.

They just got robbed.

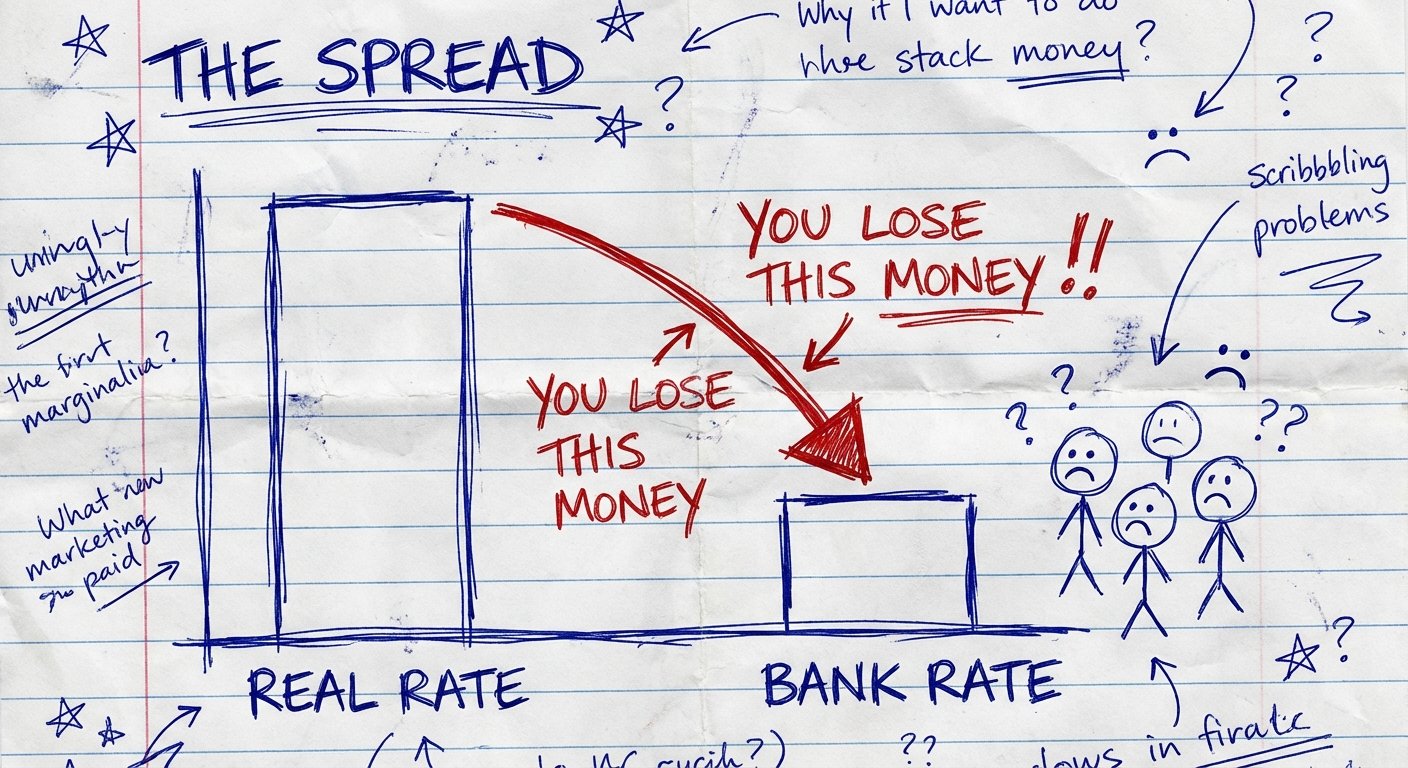

The banks don’t make money on the commission. They make money on the spread. The spread is the difference between the real exchange rate (what banks trade at) and the garbage rate they give you. It’s a hidden tax on your ignorance.

If you travel for a month and spend $5,000, a bad exchange rate costs you $250. That’s a flight upgrade. That’s five amazing dinners. That’s ROI you are flushing down the toilet because you were too lazy to set up the right infrastructure.

We are going to look at the big three: Revolut, Wise, and Charles Schwab.

I don’t care about their “brand values.” I don’t care about the color of the card. I care about the math. Which one keeps the most money in your pocket?

The Contenders: A Quick Breakdown

We aren’t comparing apples to apples here. These are three different tools for three different jobs. If you try to use a hammer to drive a screw, you’re going to have a bad time. Same logic applies here.

- Wise (formerly TransferWise): This is the utility blade. It is built for pure, transparent currency conversion. It is not a bank (technically), it is a money service business.

- Revolut: This is the lifestyle app. It tries to be a bank, a crypto exchange, and a travel agent all at once. It’s fast, slick, and has traps if you don’t read the fine print.

- Charles Schwab (High Yield Investor Checking): This is the tank. It is an old-school brokerage account attached to a checking account. It does one thing better than anyone else on earth: Cash.

1. Wise: The Transparency King

Wise changed the game. Before them, you had to guess what the exchange rate was. Wise uses the mid-market rate. This is the rate you see on Google. It is the “real” price of the money.

They make their money by charging a small, visible fee on top. Usually around 0.4% to 0.6% depending on the currency pair.

The Pros:

- No hidden markup: You get the real rate. Period.

- Multi-currency accounts: You can hold USD, EUR, GBP, and 40+ other currencies simultaneously. This is huge for freelancers or business owners. You can get paid in Euros like a local, then convert it when the rate is good.

- Physical and Digital Cards: Works everywhere Visa is accepted.

The Cons:

- ATM Fees: They are weak here. You get two withdrawals up to $100/month for free. After that, they hit you with fees. $100 is nothing. You can’t survive on that.

- Speed: Sometimes transfers to traditional banks take 1-2 days.

The Verdict:

Use Wise to send and receive money. If you are paying a contractor in Bali, use Wise. If you are receiving a client payment from London, use Wise. Do not use it as your primary cash withdrawal card.

2. Revolut: The Neobank Speedster

Revolut is aggressive. They want to be the “Super App” for everything financial. They offer stock trading, crypto, and budgeting tools. But we are here for travel.

Revolut offers interbank exchange rates (similar to the mid-market rate) during the week. This looks like “zero fees” on the surface.

The Trap (Weekend Fees):

This is where they get you. On weekends (when the markets are closed), Revolut charges a markup. usually 1%. If you land in Tokyo on a Saturday and take out cash, you are paying a fee. You have to plan ahead and exchange your money on Friday.

The Tiers:

Revolut pushes paid plans (Plus, Premium, Metal). The free plan has a limit on currency exchange (usually £1,000 or $1,000 per month depending on your region). If you go over that, they charge a fair usage fee. If you are a high roller spending $10k a month, the free plan is useless to you.

The Pros:

- Instant transfers: If your friends have Revolut, sending money is instant. Splitting bills is easy.

- Disposable Virtual Cards: This is a killer feature for security. You can generate a card number that deletes itself after one use. Perfect for booking dodgy hostels or sketchy train tickets.

- User Experience: The app is miles ahead of traditional banks.

The Verdict:

Use Revolut for day-to-day spending (swiping the card at Starbucks) and for the disposable cards. But watch the weekend fees and the monthly limits.

3. Charles Schwab: The Heavy Hitter

If you are American, this is non-negotiable. If you don’t have the Charles Schwab High Yield Investor Checking account, you are wrong.

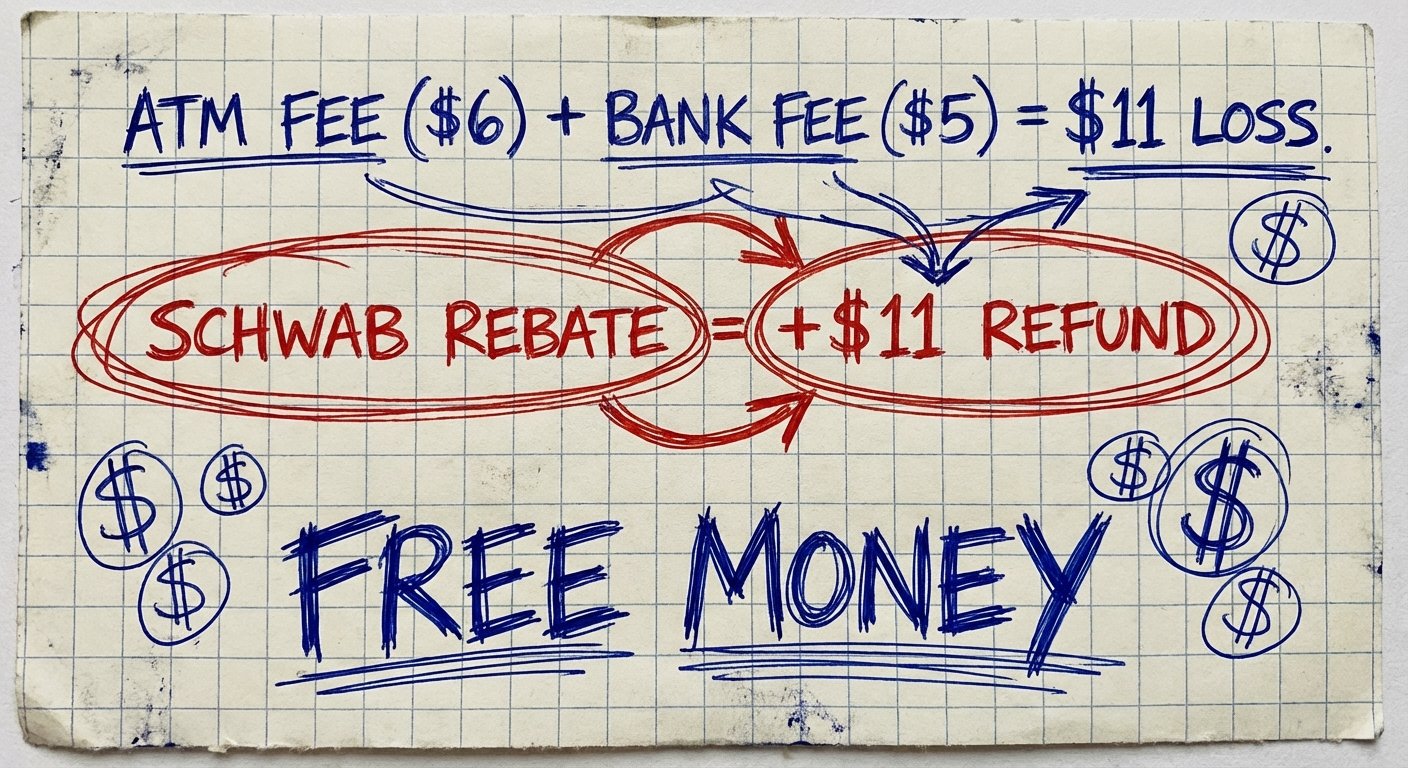

Schwab isn’t a cool tech startup. They are a massive brokerage. They don’t have a flashy app with confetti animations. They have something better: Unlimited ATM Fee Rebates.

The Math:

You go to an ATM in Thailand. The machine tells you there is a 220 Baht ($6) fee to withdraw cash. You accept it.

At the end of the month, Schwab looks at your statement, sees that $6 fee, and puts $6 back in your account.

No limits. No caps. Anywhere in the world.

I have seen people get hundreds of dollars refunded in a single trip. This is essentially free money.

The Pros:

- Zero Foreign Transaction Fees: You swipe, you pay the Visa rate. No 3% markup.

- ATM Rebates: The Global Gold Standard.

- Customer Service: You call, a human answers. A professional human. Not a chatbot.

The Cons:

- Hard Pull (Maybe): It requires opening a brokerage account (you don’t have to use it). It used to result in a hard credit pull, though reports say this is now mostly soft pulls.

- App is Boring: It’s a boomer app. It works, but it’s ugly.

The Verdict:

Use Schwab for Cash. Never use another card at an ATM. Ever.

Protecting The Asset: Hardware

You have the banking software set up. Now you need to protect the physical access. If you lose your cards, the ROI of your trip drops to zero immediately.

Do not carry your cards in a loose pocket. Do not use a $5 velcro wallet from 1999. You are an adult. Secure your assets.

You need a rigid, RFID-blocking wallet. Why? Because skimming is real in high-traffic tourist hubs. A scanner can pull your card data through your pants pocket. An RFID wallet stops the signal.

My recommendation is a rigid aluminum or carbon fiber wallet. Minimalist. Unbreakable. Holds the cards tight.

Recommendation: The Ridge Wallet (Gunmetal or Carbon)

This is the industry standard. It holds 1-12 cards without stretching out. It blocks RFID. It looks professional.

Estimated Price: $75 – $95

If you aren’t using a rigid wallet, you are asking for bent cards and compromised data. Fix it.

The “Hormozi Stack” For Travel

Stop looking for “The One Card.” It doesn’t exist. The optimal strategy is redundancy and specialization. You stack them.

Here is the exact workflow I use to ensure I never pay fees and never get stranded.

Step 1: The Hub (Wise)

I keep my liquidity in my home bank, but I move travel funds to Wise. I convert to the local currency when the rate is good (market dip). This locks in my buying power.

Step 2: The Cash Cow (Schwab)

I transfer money from Wise or my main checking to Schwab. When I land, I go to the first ATM I see. I don’t care about the fees. I take out the maximum daily limit in cash. Schwab eats the fees. Now I have local cash at the spot rate.

Step 3: The Daily Driver (Revolut/Wise)

For coffee, Uber, and restaurants, I swipe the Revolut or Wise card. If it’s a weekday, Revolut. If it’s the weekend, Wise (to avoid the 1% weekend fee on Revolut). I keep the balance on these cards low—just enough for a few days. If the card gets skimmed or stolen, the thieves only get $200, not my life savings.

The ROI Calculation

Let’s run the numbers on a $10,000 trip.

The “Average Joe” Strategy:

- Exchanges cash at airport: $1,000 @ 10% spread cost = $100 lost.

- Uses Chase Debit card for spending: $9,000 @ 3% foreign transaction fee = $270 lost.

- ATM Fees: 10 withdrawals @ $5 each = $50 lost.

- Total Loss: $420.

The “Pro” Strategy:

- Exchanges cash via Schwab ATM: $1,000 @ 0% spread + $0 ATM fees = $0 lost.

- Uses Wise/Revolut for spending: $9,000 @ mid-market rate (approx 0.5% fee baked in) = $45 cost.

- Total Cost: $45.

Net Profit: $375.

You just made $375 by spending 20 minutes setting up two bank accounts. That is a return on investment of roughly $1,125 per hour of work. If you don’t think that’s worth your time, you hate money.

Conclusion

Travel banking isn’t sexy. It’s infrastructure. And like all infrastructure, you only notice it when it breaks or costs you money.

The banks are betting on your laziness. They are betting that you won’t fill out the application form for Schwab. They are betting you won’t download Wise. They are counting on you pressing “Accept” on the bad exchange rate.

Don’t be the sucker.

1. Get Schwab for cash.

2. Get Wise for transfers.

3. Get Revolut for the interface and disposable cards.

4. Get a rigid wallet to protect the physical cards.

Set it up once. Profit forever.