This post contains affiliate links. If you purchase through our links, we may earn a small commission at no extra cost to you.

You Cannot Eat Courage

People sell you a dream. They tell you to quit your job, buy a one-way ticket, and figure it out. They say the universe will catch you.

The universe does not pay for emergency dental surgery in Thailand. The universe does not buy you a new laptop when yours gets stolen in a cafe in Colombia. Cash does.

If you run out of money as a digital nomad, you are not a nomad. You are homeless in a foreign country. That is a bad business model.

You need a runway. In the startup world, runway is how many months you can survive before the business dies. Your life is the business. You need a 6-month emergency fund before you step foot on a plane. Not three months. Not “I’ll freelance as I go.” Six hard months of cash in the bank.

Here is the exact, mathematical blueprint to build that cash buffer. No fluff. No motivational garbage. Just math and discipline.

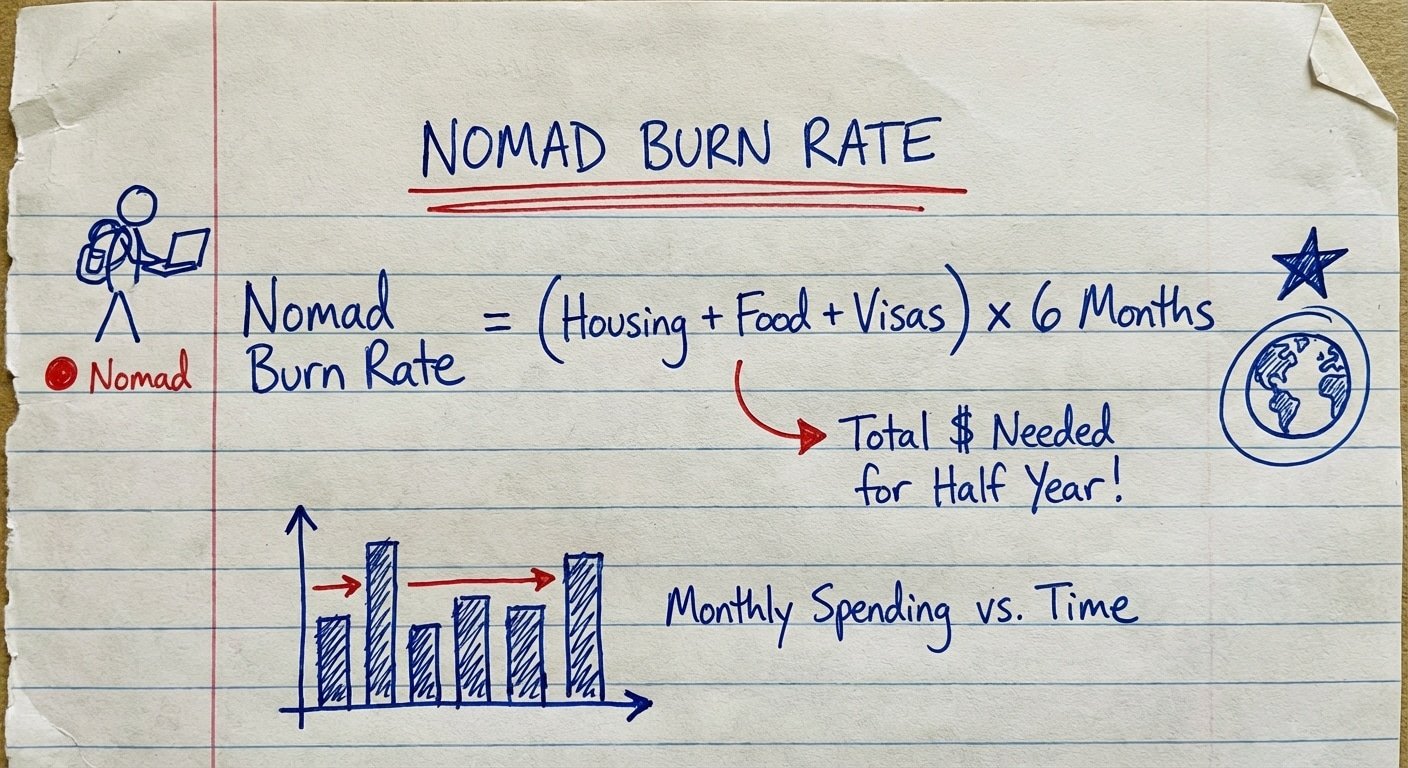

Step 1: Calculate Your True “Nomad Burn Rate”

Your current expenses do not matter. Your future expenses matter.

Most people calculate their emergency fund based on what they spend living at home. That is stupid. You are leaving home. You need to calculate your “Nomad Burn Rate.”

Your Nomad Burn Rate is the cost to survive in your target destinations, plus the cost of moving between them, plus international friction costs.

Here is what you actually need to budget for:

- Housing: Short-term Airbnb rentals cost 30% to 50% more than 12-month leases. Do not look at long-term rent prices. Look at monthly Airbnb rates.

- Food: Will you cook? Will you eat out? Pick a daily number and multiply by 30.

- Coworking: You need reliable Wi-Fi. Coffee shops are not reliable. Budget for a dedicated workspace.

- Transport: Flights, Ubers, train tickets. Moving around is expensive.

- Visas: Border runs, extensions, and tourist taxes add up.

Let’s use real numbers.

Say you want to live in Medellin, Colombia. You estimate housing is $1,000. Food is $500. Coworking is $150. Transport is $200. Flights average out to $300 a month. Visas and miscellaneous are $350. That totals $2,500 per month.

Multiply that by six. $15,000.

That is your target. Not a penny less. If you don’t have $15,000 in liquid cash, you do not get to leave. You stay home and work.

Step 2: The “Oh Sh*t” Multiplier

But wait. A 6-month emergency fund means you can survive for 6 months if your income drops to exactly zero. It does not account for massive, sudden expenses.

You need downside protection. Bad things happen when you travel. You need to plan for the worst-case scenario. I call this the “Oh Sh*t” multiplier.

Add the following to your $15,000 base:

- The “Fly Home Tomorrow” Fund: $1,500. If a family member gets sick, you need to buy a last-minute flight home from anywhere on earth. Last-minute flights are incredibly expensive.

- The “Laptop Died” Fund: $2,000. Your laptop is your money-making machine. If it breaks, you cannot wait two weeks to fix it. You buy a new one the same day.

So your real target is $18,500.

Does that sound like a lot? Good. It is. Freedom is not cheap. If you want cheap, stay in your hometown.

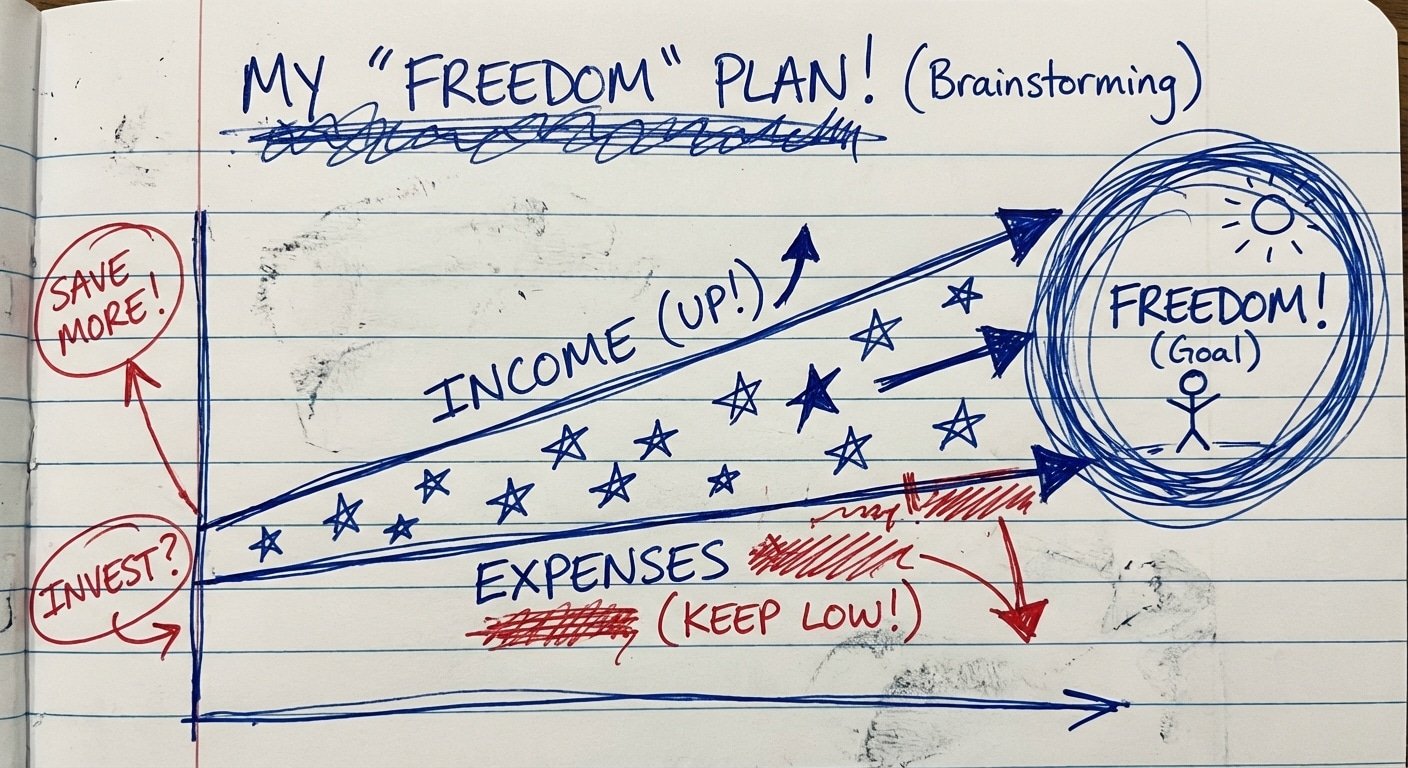

Step 3: Slashing Current Expenses (Playing Defense)

To save $18,500, you have two levers: make more, or spend less. We start by spending less because it has an immediate, guaranteed ROI.

Every dollar you do not spend is a dollar added to your runway. It is post-tax money. Saving $100 is better than earning $100, because you don’t pay taxes on savings.

You are about to leave everything behind anyway. Start living like it now.

- Break your lease: If your rent is $2,000 a month and you move into a friend’s spare room for $500 a month, you just saved $1,500 a month. In six months, that is $9,000. Half your emergency fund is done.

- Sell your car: Cars are depreciating liabilities. Sell it. Put the cash straight into the fund. Take the bus. Ride a bike. Stop paying for gas, insurance, and parking.

- Cancel every subscription: Netflix, Spotify, gym memberships. You want to travel the world? Go run outside. Read books from the library. Cut the fat.

People complain they cannot save money, yet they live alone in a nice apartment, drive a financed car, and eat out four times a week. They don’t want freedom. They want comfort. You cannot have both in the beginning.

Step 4: Liquidating Your Crap

Look around your room. Everything you own is trapped cash. You are paying rent to store things you will not take with you.

Turn your liabilities into liquidity.

Sell the TV. Sell the gaming console. Sell the designer clothes. Sell the expensive furniture. You only need a backpack when you leave.

If you sell $3,000 worth of stuff, you just bought yourself more than a month of runway. You traded useless plastic for a month of breathing room in a foreign country. That is a highly profitable trade.

Step 5: Increasing Cash Inflow (Playing Offense)

You can only cut so much. Eventually, you hit a floor. But your earning potential has no ceiling.

If you want to build this fund fast, you need more cash flowing in. If you have a 9-to-5, you work from 6 PM to midnight. You work weekends. You trade your free time for cash.

Pick a high-ROI side hustle. Do not drive Uber. The margins are terrible after gas and wear-and-tear. Do something that builds a skill you can use on the road.

- Freelance writing.

- Video editing.

- Virtual assistance.

- B2B Lead generation.

These are skills that require zero startup capital. You just need a laptop and relentless outreach. Send 100 cold emails a day. Offer to work for free to get a case study. Then charge the next guy. If you make an extra $1,500 a month on the side, you accelerate your timeline drastically.

Step 6: Protecting Your Digital Assets

Before we talk about where to put your money, we need to talk about protecting the very thing that makes you money. Your gear.

If you lose your data, you lose your clients. If you lose your clients, your income goes to zero. Your emergency fund will start draining immediately.

Do not trust the cloud alone. Wi-Fi in remote places drops. You need physical, rugged backups. A flimsy hard drive will break in your backpack. Buy a professional-grade solid state drive. Period.

I highly recommend the SanDisk 2TB Extreme Portable SSD. It is drop-resistant, water-resistant, and incredibly fast. It costs around $130 – $160. Buy it, back up your entire business, and keep it in a separate bag from your laptop.

Spending $150 now prevents a $10,000 loss in client revenue later. That is called risk mitigation. Amateurs ignore it. Professionals mandate it.

Step 7: Where to Park the Cash

You have the $18,500. Where does it go?

Do not leave it in your local checking account. If you do, inflation eats it, and your bank will freeze it the second you try to buy a coffee in Vietnam.

You need to structure your finances for a global lifestyle.

First, put the bulk of the money ($15,000) into a High-Yield Savings Account (HYSA). You want that money earning 4% to 5% interest while it sits there. That is $600 to $750 a year in free money. It pays for your flights.

Second, you need a multi-currency setup. Traditional banks charge you 3% foreign transaction fees and give you terrible exchange rates every time you swipe your card. Over six months, that could cost you thousands of dollars.

You need Wise. Wise gives you local bank details in multiple countries. You get the real mid-market exchange rate. No hidden markups. No BS fees. Keep your daily operating cash here, and instantly convert it to the local currency of whatever country you are in.

Step 8: Bulletproofing Your Health

An emergency fund is for predictable emergencies. Lost income. Broken gear. Bad travel logistics.

It is NOT for a $50,000 hospital bill because you crashed a scooter in Bali.

If you rely on your cash buffer to pay for major medical emergencies, you are playing Russian roulette with your financial life. One bad accident will bankrupt you.

You need travel medical insurance. It is non-negotiable.

Do not use regular health insurance from your home country. It will not cover you abroad. Do not rely on credit card travel insurance. It only covers short trips and has massive loopholes.

Use SafetyWing. They built insurance specifically for digital nomads. It functions like a subscription. You pay month-to-month. It covers you in almost every country on earth. If you get sick, if you get into an accident, if you need a medical evacuation, they cover it. It costs roughly $45 to $55 for four weeks.

Paying $50 a month to protect your $18,500 emergency fund from being wiped out by a medical bill is the easiest ROI decision you will ever make.

Step 9: Securing Your Network

We covered your hardware. We covered your health. Now we cover your data flow.

When you are a nomad, you will connect to hundreds of public Wi-Fi networks. Airports. Airbnbs. Cafes. Coworking spaces.

Public Wi-Fi is a playground for hackers. If someone intercepts your connection, they get your passwords. They get your bank logins. They drain your accounts. Your emergency fund is gone in ten seconds.

You must encrypt your connection. Always.

Use NordVPN. It hides your IP address and encrypts your internet traffic. It also lets you route your connection through your home country, which stops your bank from locking your accounts when you log in from abroad. It is cheap, fast, and secure.

Again, downside protection. You spend a few dollars a month to protect tens of thousands. Do the math.

The Psychology of the Cash Buffer

Building this fund will be hard. It will take time. You will see other people posting photos from beaches while you are stuck in your hometown saving pennies.

Ignore them.

Half of those people are drowning in credit card debt. The other half will be forced to fly home in three months when their clients churn and they can’t make rent.

When you finally leave, you will have something they do not have: Peace of mind.

When a client fires you, you will not panic. You have six months of runway. You can take your time to find a better client.

When you get burned out, you can stop working for a month. You can sit on a beach and do absolutely nothing. Your fund pays for it.

Money is a tool. It buys options. It buys time. When you have a massive cash buffer, you operate from a position of strength. You don’t take bad deals. You don’t tolerate bad clients. You make rational, long-term decisions.

When you are broke, you are desperate. Desperate people make bad decisions. They take cheap clients. They work 80-hour weeks just to survive. They trade a cubicle in their home country for a laptop cage in a tropical country. That is not freedom.

Summary of the Blueprint

Let’s review the exact steps:

- Step 1: Calculate your monthly survival cost in your target country.

- Step 2: Multiply it by six. Add $3,500 for emergency flights and broken gear.

- Step 3: Slash your living expenses immediately. Move to a cheaper place. Sell your car. Cancel everything.

- Step 4: Sell all your useless stuff for fast cash.

- Step 5: Start a side hustle to increase your monthly income. Save 100% of the profits.

- Step 6: Buy physical backups for your data.

- Step 7: Put the money in a High-Yield Savings Account and use Wise for international spending.

- Step 8: Buy nomad medical insurance so a hospital bill doesn’t bankrupt you.

- Step 9: Secure your internet connection with a VPN.

Do not skip steps. Do not negotiate with the math. Do the work. Save the money. Buy your freedom.

Your future self will thank you when the inevitable happens, and instead of a tragedy, it is just an inconvenience.