The Math Behind Medical Risk: Why Most Nomads Are Betting Against Themselves

Most people treat travel insurance like a charity donation. They throw money at a company and hope they never see it again.

This is the wrong way to look at it.

Insurance is financial leverage. It is purchasing a capped downside for a fixed monthly cost. That is it.

If you are a digital nomad or remote entrepreneur, your body is your primary asset. If that asset breaks in a foreign country without a service contract (insurance), you go to zero. I see people making $10k a month risking bankruptcy over a $50 monthly premium. It makes no sense.

You want the highest coverage for the lowest friction and the lowest cost.

I looked at the data. I compared the three biggest players: SafetyWing, World Nomads, and Genki.

Here is who wins, who loses, and who is ripping you off.

The Three Contenders

We are looking at three specific providers. They all promise the same thing: they pay the bill when you get sick. But the mechanics—and the ROI—are different.

- SafetyWing: The low-cost, automated solution.

- World Nomads: The legacy brand. High cost, high coverage.

- Genki: The new European challenger.

Let’s break them down by the numbers.

1. SafetyWing (Nomad Insurance 2.0)

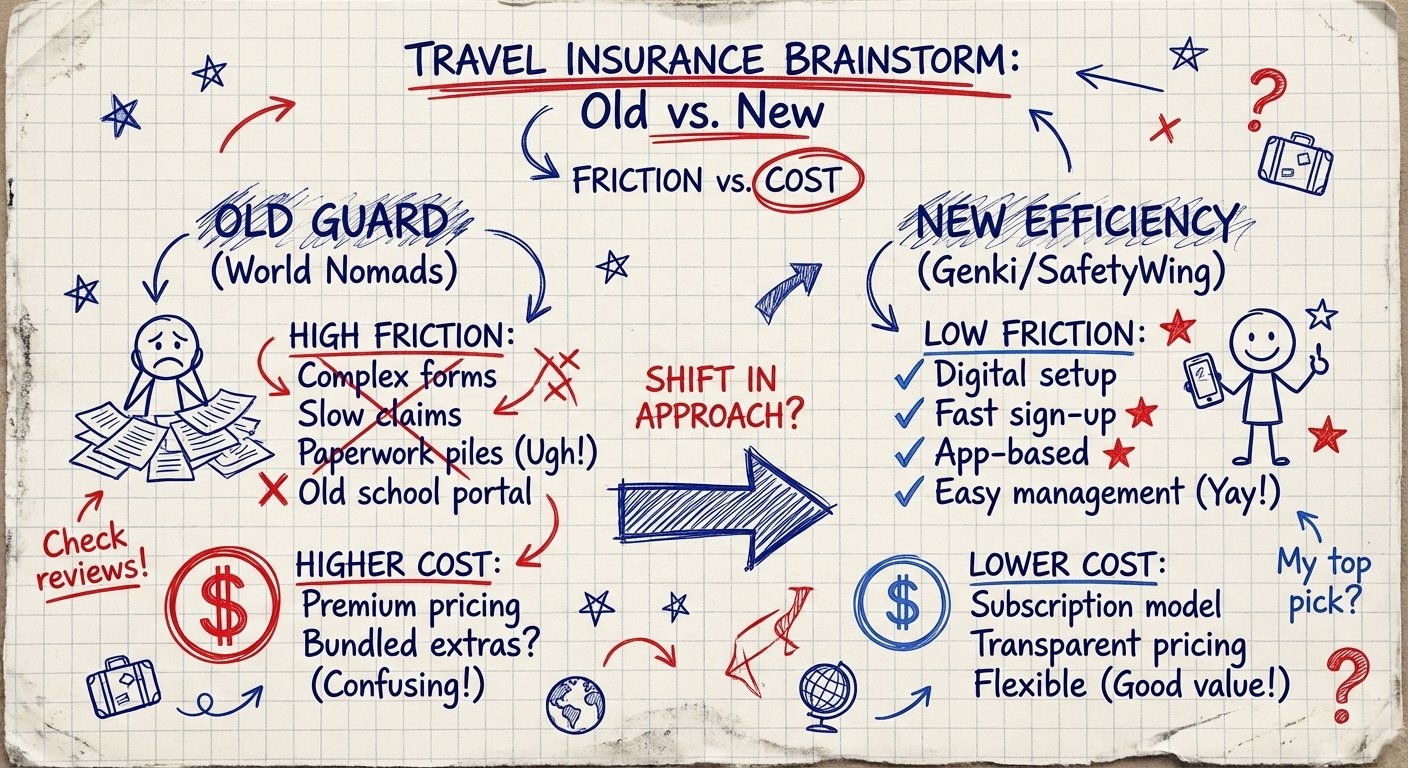

SafetyWing built their entire business model on one thing: Friction reduction.

They know you hate paperwork. They know you forget to renew. So they made a subscription model. You turn it on. It charges you every 28 days. You turn it off when you get home.

The Numbers (Ages 10-39):

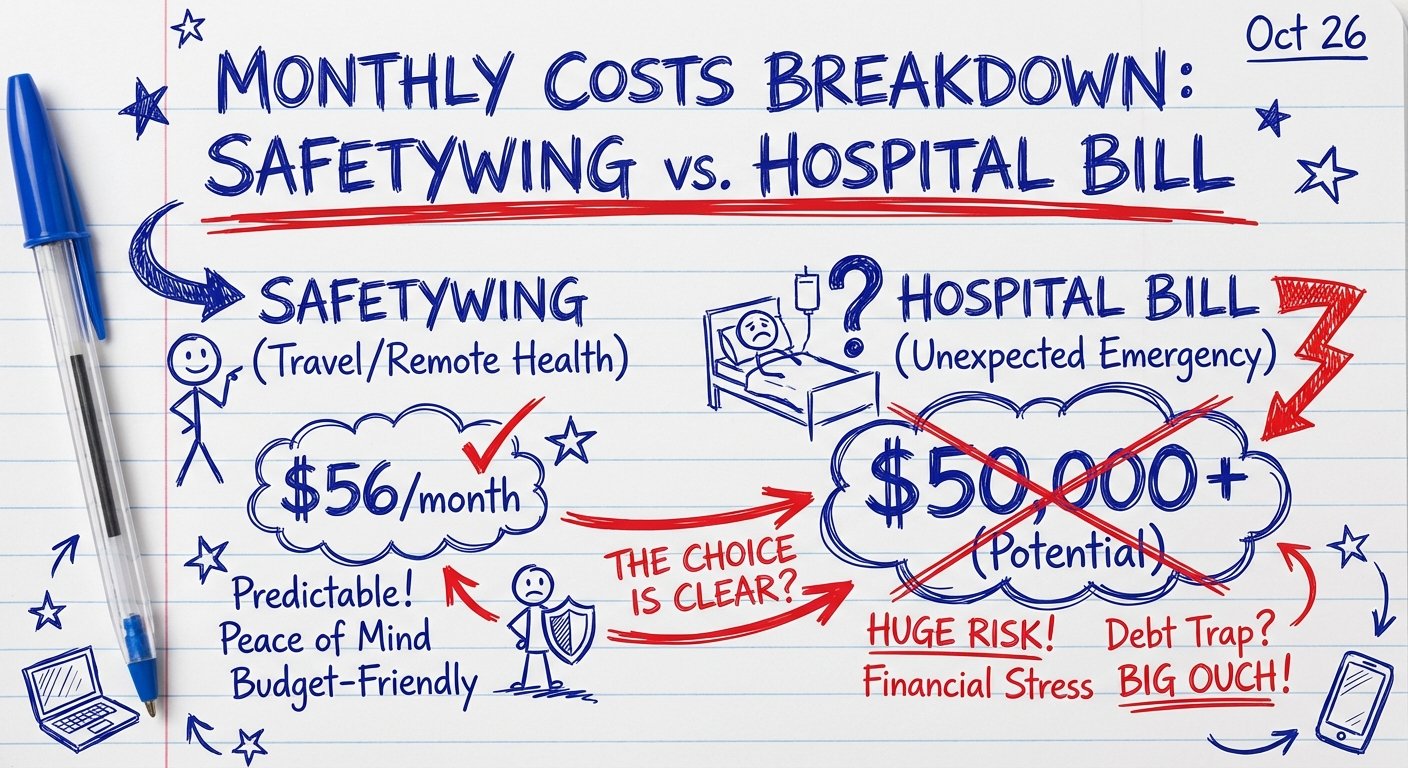

- Price: ~$56.28 per 4 weeks (excluding US travel).

- Deductible: $250.

- Max Limit: $250,000.

The Pros:

It is cheap. It is automated. If you are healthy and just want “catastrophe coverage” so you don’t go bankrupt from a scooter accident in Bali, this is the highest ROI choice. They recently updated to “2.0” which improved their claims handling time, which used to be terrible.

The Cons:

The $250 deductible means you pay for your own minor doctor visits. If you get the flu and the visit is $150, you pay it. SafetyWing is for the big stuff.

2. World Nomads

World Nomads is the “Old Guard.” They have been around forever. Because of that, they charge a premium. You are paying for the brand.

They market heavily to adventure travelers. If you are skydiving, heli-skiing, or shark wrestling, World Nomads usually has a tier that covers it.

The Numbers:

- Price: Highly variable. Usually $120 – $200+ per month depending on destination.

- Deductible: Varies, often $100+.

- Max Limit: Often higher than SafetyWing, depends on the plan (Standard vs. Explorer).

The Logic:

For 95% of digital nomads sitting in coffee shops, this is a bad deal. You are overpaying for risk coverage you don’t need. You are paying double or triple the premium of SafetyWing.

However, if you are filming a documentary on the side of Everest, the ROI shifts. You need the specialized “Explorer” coverage. For the average laptop worker, this is burning cash.

3. Genki (The New Efficiency)

Genki is interesting. They are backed by heavy German underwriting (Allianz and Dr. Walter). Germans do not mess around with insurance.

They offer two products: Genki Explorer (Travel health insurance) and Genki Native (Comprehensive international health insurance).

We are looking at Genki Explorer.

The Numbers:

- Price: Starts around €48 – €65 per month (approx $50-$70 USD).

- Deductible: €50 per case (or €0 options available).

- Coverage: Includes some sports that others exclude.

The Verdict:

Genki is aggressive. They are trying to undercut SafetyWing on quality while matching the price. Their terms are clearer. They function more like “Health Insurance” and less like “Emergency Travel Assistance.”

The “Physical Risk” Factor (Stuff You Need)

Insurance covers your body. It usually sucks at covering your gear. High-value item coverage on these plans is often capped at $500 per item or has massive loopholes.

If you drop your $3,000 MacBook Pro, SafetyWing is not going to buy you a new one quickly.

You need to mitigate physical risk yourself. This means buying protection for your hardware so you don’t have to make a claim in the first place. The best insurance is not breaking your stuff.

Recommended Gear Protection:

Don’t use a cheap backpack. Get a weather-resistant, crush-proof travel bag for your tech.

Price Range: $150 – $250

Also, if you are traveling solo, stop assuming you will be conscious to tell the doctors your medical history. Wear a digital ID or carry a localized medical kit.

Price Range: $30 – $60

The Head-to-Head Comparison

Here is the reality of the market right now.

SafetyWing vs. Genki

This is the real battle. World Nomads is too expensive for the general market.

SafetyWing wins on convenience. The UI is better. The subscription is seamless. If you are moving constantly, it just works.

Genki wins on the fine print. Their medical coverage is slightly more robust for the same price point. However, their sign-up process feels a bit more like a traditional German contract.

Who Wins? The ROI Verdict

We make decisions based on outcome per dollar spent.

Winner 1: The “Set and Forget” Nomad

Pick: SafetyWing.

You want to spend zero minutes thinking about this. You want to pay ~$56, get the PDF, and get back to work. The cost is negligible compared to your income. It caps your downside. Speed is wealth.

Winner 2: The “Optimizer” / Long Term

Pick: Genki.

You plan to stay in Europe or Asia for 1-2 years. You want lower deductibles. You are willing to read a few more pages of terms to save $100 a year in potential copays. The German backing provides high security.

Loser: The Brand Loyalist

Avoid: World Nomads (Unless absolutely necessary).

Unless you are doing high-risk extreme sports that the others specifically exclude, you are lighting money on fire. The premium does not match the value for a standard laptop worker.

Final Logic

Do not overthink this. Analysis paralysis costs you money.

If you leave your home country without insurance, you are accepting infinite risk for a $50/month saving. That is bad business. That is bad math.

1. Pick one.

2. Set up auto-pay.

3. Go make money.

Disclaimer: I am not an insurance broker. I am a business operator. Read the policy wording (PDS) yourself before buying. Terms change. Don’t be lazy.